Smart shifts, rising values, and what to watch next

Australia’s housing market continues its steady and strategic rise, with new data from CoreLogic and NAB revealing signs of confidence, resilience, and long-term opportunity. Although affordability remains a challenge in some sectors, the broader trends suggest we’re in a balanced, forward-looking market that rewards planning over panic.

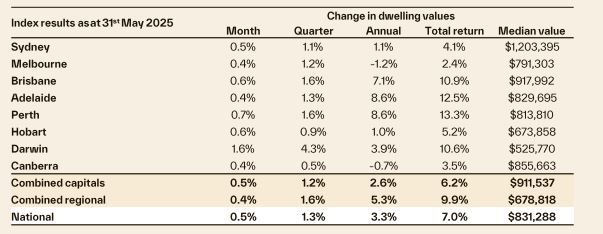

National Dwelling Values Still Rising

According to CoreLogic, Australian dwelling values rose by 0.5% in May, bringing the year-to-date increase to 1.7%. Over the quarter, growth has held firm at 1.3%, and annual price growth has eased to 3.3%.

This moderation signals a shift from the volatility of previous years into a more stable market rhythm. It’s no longer about chasing short-term gains – now, it’s about identifying sustainable value.

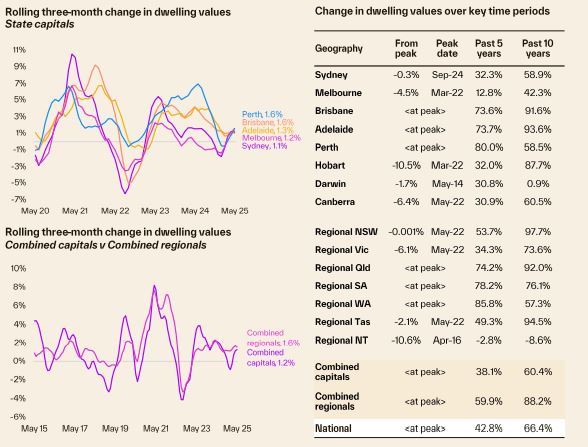

Capital Cities: Growth Converges

Growth conditions across the capital cities are beginning to align. Darwin led Q2 with a +4.3% quarterly increase, followed by Perth and Brisbane at +1.6%. Sydney, Melbourne, Adelaide, and Canberra also recorded modest growth.

What’s significant is the narrowing gap: the range between the highest and lowest annual growth in dwelling values across capital cities has tightened to just 9.8 percentage points – the most consistent spread since March 2021. This convergence suggests greater predictability and less volatility across metro markets.

Rental Yields: Slower Growth, Tighter Market

The national rental market is softening – but not weakening. Rents rose 0.4% in May, after three months of stronger 0.6% gains.

Annual trends show a broad slowdown in growth across most capitals, particularly Sydney and Melbourne, which are now the softest rental markets after a period of sharp rises. By contrast, Darwin and Hobart are still seeing upward rental pressure.

This slowdown is happening despite record-low vacancy rates, which remain below 2% in every capital – well under the decade average of 2.6%.

So, how can rental growth ease if there’s still low supply?

It comes down to affordability pressures and a cooling in net overseas migration. Many renters have reached their limit, and we’re now seeing larger households form – including shared housing and multi-generational living – which absorbs demand.

On top of that, the COVID-era surge in overseas migration is tapering off, with fewer new renters entering the market and more temporary visa holders returning overseas.

What’s Next: Economic Signals and Policy Outlook

According to NAB and CoreLogic, the Reserve Bank of Australia is becoming more comfortable with inflation trends. Core inflation is expected to sit within the 2–3% target range until mid-2027 – paving the way for further interest rate cuts.

- NAB expects the cash rate to fall to 3.1% by August, and 2.6% by early 2026

- The unemployment rate is forecast to rise to 4.3% by year-end

- GDP growth remains modest, at 2.1% for 2025

Meanwhile, political certainty following the federal election and the planned expansion of the 5% deposit scheme for first-home buyers in 2026 could further support market confidence – even before the scheme kicks in.

However, housing affordability remains a key constraint. At the end of 2024, the national dwelling value to household income ratio sat at 8.0, while serviceability costs remain near record highs. Lending restrictions and slowing population growth will also act as checks on runaway price growth.

Your Next Smart Move

Whether you’re buying, investing, or exploring your options, now is the time to get your strategy right.

Reach out to Wealthology today. We’ll help you find clarity, spot opportunity, and take the next step with confidence.

Let’s build wealth your way – smart, sustainable, and data-driven.

And watch this space – we’ll be releasing more insights and updates as Q3 unfolds. Don’t miss the next wave.

Discover more insights on these topics:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}